By Hardik Gupta

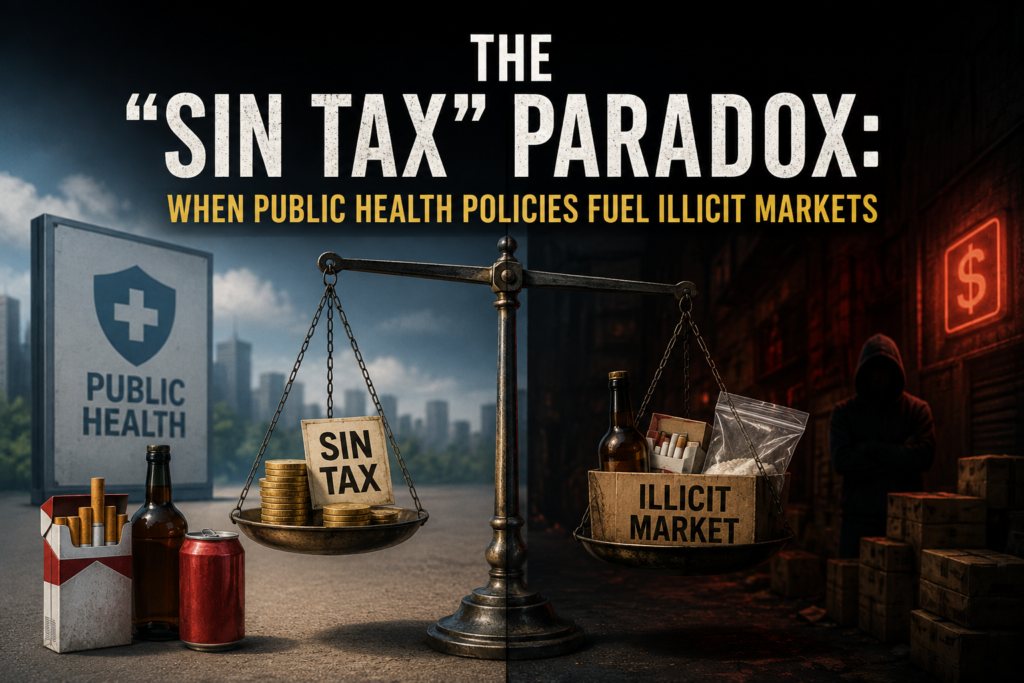

Governments across the world impose higher taxes on products such as tobacco, alcohol, sugary beverages, cannabis, and gambling. Commonly known as “sin taxes,” these excise duties are intended to discourage the consumption of products considered harmful to public health while simultaneously generating revenue to offset the social and healthcare costs arising from their use.

The rationale appears straightforward: as the price of a harmful product increases, consumers are expected to purchase less of it. However, the practical consequences are often far more complex. While higher taxes may reduce legal sales, they can also create profitable opportunities for illegal trade. This raises an important legal and policy question, when does an effective public health measure begin to encourage tax evasion, smuggling, and organised crime?

The Legal Basis of Sin Taxes

The power to levy taxes is one of the sovereign functions of the State. Excise duties on harmful products are not imposed merely to generate revenue; they also represent an exercise of the State’s police power to protect public health, safety, and welfare.

From an economic perspective, these taxes are based on the Pigouvian tax principle, named after economist Arthur Pigou. The principle seeks to address negative externalities costs imposed on society because of an individual’s private choices.

For example, tobacco consumption often results in long-term healthcare expenses that are ultimately borne by the public. By imposing higher taxes on cigarettes, the law attempts to ensure that consumers bear a greater share of these societal costs rather than shifting the burden to taxpayers. Courts across several jurisdictions have consistently upheld such taxes, recognising that discouraging harmful behaviour through fiscal policy serves a legitimate public purpose

Do Higher Taxes Actually Reduce Consumption?

In many cases, sin taxes have successfully reduced the consumption of harmful products, particularly among younger and price-sensitive consumers. Increased taxation on tobacco products and sugary drinks has frequently been accompanied by a decline in legal sales.

However, a reduction in legal sales does not always mean that overall consumption has decreased. The effectiveness of a sin tax largely depends on the nature of the product.

1. Product with Readily Available Alternatives

Products such as sugary drinks are generally more responsive to price increases. Consumers can easily switch to alternatives such as water, fruit juices, or sugar-free beverages. In such cases, taxation often achieves its intended public health objective without significantly disrupting the market.

2. Addictive Products

The situation is very different for addictive commodities such as tobacco, alcohol, or narcotic substances. Because these products create physical or psychological dependence, consumers are less likely to stop purchasing them solely because prices have increased.

Instead, many users begin searching for cheaper alternatives, including products available through illegal channels. This is where the effectiveness of taxation begins to diminish.

When Higher Taxes Encourage Illegal Trade

The greatest challenge arises when excise duties become disproportionately high compared to the actual cost of manufacturing the product. The wider this price difference becomes, the more profitable it is for criminal networks to evade taxes and supply cheaper goods through illegal markets.

High Excise Duty → Higher Retail Price → Greater Profit from Tax Evasion → Expansion of Illegal Markets

At this stage, the law may unintentionally create incentives for illicit commerce rather than discourage consumption.

1. Smuggling & Tax Evasion

Significant differences in tax rates between neighbouring States or countries often encourage cross-border smuggling.

A frequently cited example is the substantial difference in cigarette taxes between certain American states, where organised criminal groups purchase tobacco in low-tax jurisdictions and illegally transport it into high-tax jurisdictions for resale.

What begins as a public health measure therefore evolves into a law enforcement issue involving offences such as tax evasion, smuggling, money laundering, racketeering, and organised crime.

2. Counterfeit & Unsafe Products

High taxation also creates demand for counterfeit products that completely bypass regulatory controls.

To avoid paying excise duties or complying with tax-stamp requirements, illegal manufacturers frequently produce unregulated alcohol and tobacco products. These products escape government quality inspections and often contain dangerous substances.

Consumers may therefore be exposed to counterfeit alcohol containing toxic levels of methanol or tobacco contaminated with harmful chemicals. Ironically, the very policy intended to protect public health may expose consumers to even greater health risks.

3. The Regressive Nature of Sin Taxes

Another criticism frequently raised is that sin taxes disproportionately affect lower-income households.

Since low-income consumers spend a larger share of their earnings on essential and addictive goods, they bear a heavier financial burden when excise duties increase. Those who cannot afford legally taxed products may be driven towards illegal markets, increasing their exposure to criminal networks and legal consequences.

This creates concerns not only about economic inequality but also about the unequal impact of criminal enforcement.

4. Finding the Right Regulatory Balance

The challenge for legislators is not whether sin taxes should exist, but how they should be designed.

An effective legal framework requires more than simply increasing tax rates. Moderate and gradual tax increases should be accompanied by strong enforcement measures, including robust supply-chain monitoring, digital track-and-trace systems, strict penalties for illicit distributors, and coordinated action against organised smuggling networks.

Equally important is ensuring that revenue generated through sin taxes is meaningfully utilised. If the primary objective is public health, a substantial portion of the proceeds should be allocated towards awareness campaigns, de-addiction programmes, medical treatment, and rehabilitation initiatives rather than serving merely as a source of general revenue.

Conclusion

Sin taxes remain one of the most important regulatory tools available to governments for discouraging harmful behaviour and promoting public health. However, taxation alone cannot achieve these objectives.

If tax rates become excessive without adequate enforcement and public health support, they may unintentionally encourage black markets, counterfeit goods, and organised crime. The effectiveness of a sin tax therefore depends not on how heavily a product is taxed, but on whether taxation forms part of a balanced legal framework that combines fiscal policy with effective regulation, enforcement, and public welfare measures.

Ultimately, the success of a sin tax lies in striking the right balance between protecting public health, preserving market integrity, and ensuring that the law does not create incentives for the very illegal activities it seeks to prevent.